Wall Street Pulls Back From a Money-Spinning Bitcoin Trade

In this article: BTC-USD

CME

Coinglass

(Bloomberg) -- A quiet but telling shift is unfolding in the crypto derivatives market, as one of the most reliable money-making trades shows signs of breaking down.

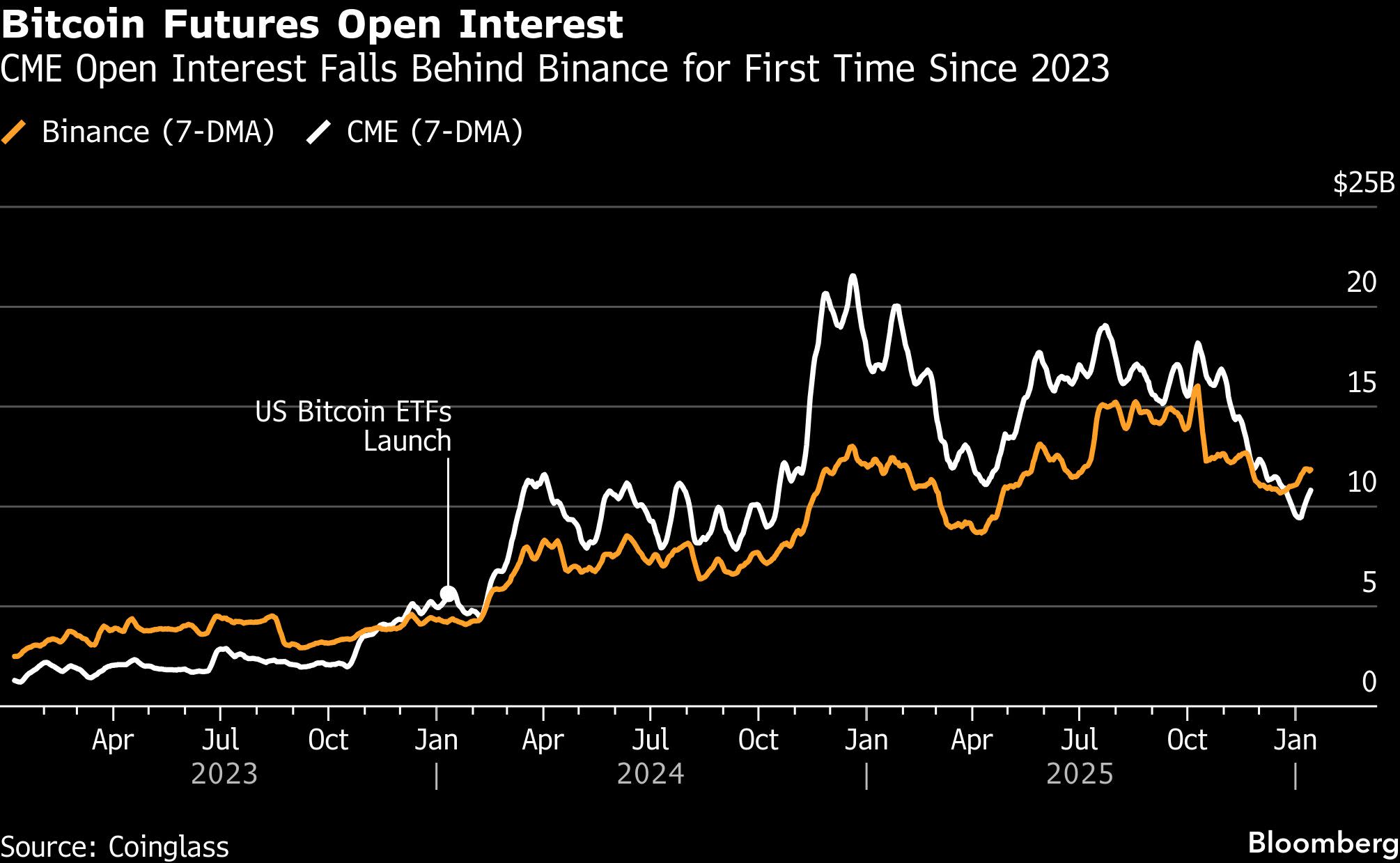

The cash-and-carry trade — in which institutions bought spot Bitcoin and sold futures to capture pricing gaps — is collapsing and signaling a deeper shift in crypto’s market structure. Open interest in Bitcoin futures on the Chicago Mercantile Exchange has slipped below Binance’s for the first time since 2023, underscoring how tighter spreads and more efficient market access are eroding a once-lucrative arbitrage.

Most Read from Bloomberg

Tokyo Becoming Colony for the Rich, Pritzker Winner Warns

New York City’s Worst Highways Can Lead Somewhere Better

NYC Bans Hidden Hotel Fees Ahead of World Cup Tourist Influx

The CME Group Inc.’s exchange had been the venue of choice for Wall Street desks running these trades after spot Bitcoin ETFs launched in early 2024. The setup, mirroring the basis trade in traditional markets, was simple: buy spot Bitcoin via ETFs, sell futures, and collect the spread.

In the months following ETF approvals, annualized returns on the so-called delta-neutral strategy often hit double digits, drawing billions from funds that didn’t care about price direction — only yield. But the ETFs that supercharged the trade also sowed its demise: as more desks piled in, the arbitrage spread collapsed. Now, the trade barely clears the cost of capital.

One-month annualized yields are hovering around 5%, among the lowest in years, according to data compiled by Amberdata. Greg Magadini, director of derivatives at Amberdata said that the basis was closer to 17% this time last year and now sits near 4.7%, barely clearing the hurdle set by funding and execution costs. With one-year Treasuries yielding about 3.5%, the trade’s appeal is fading fast.

Amid the basis compression, CME Bitcoin futures open interest has fallen below $10 billion from a peak of over $21 billion, while Binance’s open interest has been steady at around $11 billion, according to data compiled by Coinglass. The shift reflects a pullback from hedge funds and larger US accounts rather than a wholesale retreat from crypto since prices peaked in October, according to James Harris, chief executive officer of digital asset management firm Tesseract.

Crypto exchanges like Binance are the main venue for perpetual futures, a type of contract on which settlement, pricing, and calculation of margin is done on an ongoing basis, often multiple times a day. Perps, as they’re known, account for the largest trading volumes in the crypto market. Last year, CME also started smaller-sized, longer-dated futures contracts for cryptoassets and equity-index markets offer futures positions in spot-market terms, allowing investors to hold contracts for up to five years without rolling into a new contract.

“CME has historically been the venue of choice for institutions and cash and carry arbitrage,” Harris said, adding that the crossover with Binance “is a meaningful signal about how market participation is shifting.” He described the moment as a “tactical reset,” driven by muted yields and thinning liquidity rather than a loss of conviction.

As per a note shared by the CME Group, 2025 was an inflection point in the market as growing regulatory clarity improved investor outlook in the space, which saw institutions diversifying beyond Bitcoin into tokens like Ether, Ripple’s XRP and Solana.

“We averaged around $1 billion in daily notional OI for Ether in 2024, and in 2025 that number increased to almost $5 billion,” CME Group said.

Even as Federal Reserve rate cuts have lowered funding costs, that has failed to spark a sustained rally in crypto ever since token prices crashed across the board on Oct. 10. Borrowing demand is softer, decentralized finance yields are low, and traders are favoring options and hedges over outright leverage.

Le Shi, Hong Kong managing director at market maker Auros, said that as markets mature, traditional players now have more avenues — from ETFs to direct exchange access — to express directional views. That choice narrows price gaps between venues and naturally squeezes the arbitrage that once inflated CME open interest.

“There’s a self-balancing effect,” Le said, arguing that as participants gravitate to the cheapest venue, the basis shrinks and the incentive to run carry trades diminishes.

Bitcoin fell as much as 2.4% to $87,188 on Wednesday, before paring the loss. The decline briefly erased all the gains registered since the start of the year.

The era of near-riskless high returns is likely over, pushing traders toward more complex strategies in decentralized markets, according to Bohumil Vosalik, CIO of 319 Capital. For high-frequency and arbitrage-focused firms, that means hunting elsewhere, he said.

(Update the price of Bitcoin.)

Most Read from Bloomberg Businessweek

I’ve Studied How Democracies Fail. Here’s My Unified Theory of Trump

The Economic Toll of Trump’s Policies Will Soon Be Visible

Janet Yellen Says Trump’s Moves Against Powell Are Backfiring

A Global Explosion of Absurdly Spicy Foods

Industry TV Recap: Failing Upward, Right to the Boardroom

©2026 Bloomberg L.P.

Recent

News

Newsletter

Subscribe to our mailing list to get the new updates!

Subscribe our newsletter to stay updated

Most

Reviews

Markets

- Wed, 28 Jan 2026

HCI Group (HCI) Gains As Market Dips: What You Should Know

Economy

Finance

- Tue, 20 Jan 2026

Why the Trump administration is going to Davos

Markets

Top Stories